In today’s rapidly evolving financial landscape, digital banks are transforming the way we manage our finances. Understanding how these online-only banks operate is crucial for anyone looking to navigate the modern banking world. This article will delve into the inner workings of digital banking, exploring the technologies they utilize, the services they offer, and the benefits and challenges they present to consumers. From mobile banking apps to online account management, we’ll cover the key features that define the digital banking experience. We will explore how digital banks operate differently from traditional banks, highlighting their unique characteristics and the implications for customers.

Digital banks, also known as virtual banks or online banks, leverage technology to streamline financial operations and provide convenient banking services. We’ll examine how they utilize automation, artificial intelligence, and data analytics to enhance efficiency and personalize the customer experience. Additionally, we’ll explore the various types of digital banking platforms and the different business models they employ, including neobanks, challenger banks, and partnerships between traditional banks and fintech companies. This comprehensive overview will equip you with the knowledge necessary to understand how digital banks operate and make informed decisions about your financial future.

What Is a Digital Bank?

A digital bank is a financial institution that delivers banking services primarily through online and mobile platforms. Unlike traditional banks with physical branches, digital banks operate virtually, offering customers access to their accounts and financial tools anytime, anywhere.

These banks offer a wide range of services, often including account opening, money transfers, bill payments, and even investment options. Customers interact with the bank through user-friendly apps and websites, eliminating the need for in-person visits.

How Digital Banks Differ from Traditional Banks

Digital banks distinguish themselves from traditional banks primarily through their operational model and service delivery. While traditional banks rely heavily on physical branches, digital banks operate exclusively online, offering services through websites and mobile applications. This key difference translates to a generally lower cost structure for digital banks, often passed on to customers through reduced fees and higher interest rates on savings accounts.

Another key differentiator lies in accessibility. Digital banks offer 24/7 service availability, enabling customers to manage their finances anytime, anywhere. Traditional banks are limited by branch operating hours, offering less flexibility.

Finally, digital banks often leverage technology to provide innovative features such as automated budgeting tools and personalized financial advice. While some traditional banks are beginning to integrate similar technologies, digital banks generally lead in this area.

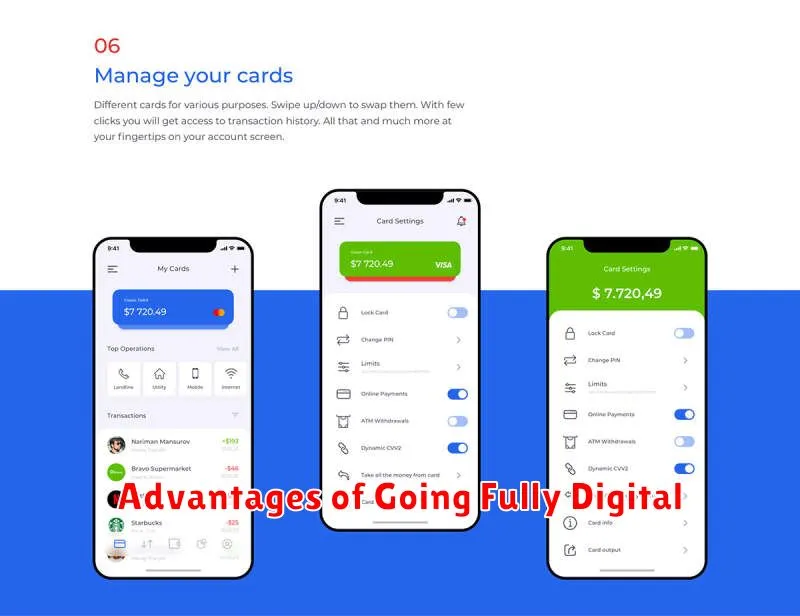

Advantages of Going Fully Digital

Embracing a fully digital banking experience offers several key advantages for customers. Convenience is paramount, with 24/7 account access and the ability to conduct transactions from anywhere. This eliminates the need for physical branch visits and expands banking accessibility.

Lower fees are often associated with digital banks due to reduced overhead costs. These savings can be passed on to customers in the form of lower or nonexistent monthly maintenance fees, ATM fees, and overdraft charges.

Higher interest rates on savings accounts are another potential benefit. Digital banks may offer more competitive rates compared to traditional institutions, helping customers grow their savings faster. Innovative features, such as automated budgeting tools and personalized financial insights, can also enhance the overall banking experience.

Speed and efficiency are additional advantages. Transactions are processed quickly and efficiently within digital platforms. Account updates and statements are readily available, enabling real-time monitoring of finances.

Common Features of Digital Banking

Digital banking platforms offer a range of services designed for convenient financial management. Account access is a core feature, allowing users to monitor balances, transaction history, and statements. Money transfers, both domestically and internationally, are typically facilitated through various methods.

Bill payment services automate recurring expenses and provide payment reminders. Mobile check deposit eliminates trips to physical branches, allowing users to deposit checks via their mobile devices. Many platforms also offer budgeting and financial management tools to help users track spending and savings goals.

Customer support is usually provided through secure messaging, email, or phone calls, often available 24/7. Some platforms also offer virtual financial advisors for personalized financial guidance.

Are Digital Banks Safe?

Security is a primary concern for many considering digital banking. While no banking system is entirely impervious to risk, digital banks employ various security measures to protect customer funds and data. These often include encryption, multi-factor authentication, and biometric logins.

Furthermore, many digital banks are regulated by the same authorities as traditional banks, requiring them to adhere to similar security standards and practices. This oversight helps ensure a level playing field and provides customers with a degree of confidence. However, it’s crucial to choose a reputable digital bank with a proven track record and transparent security protocols.

User Verification and KYC in Digital Banks

User verification and Know Your Customer (KYC) checks are crucial aspects of digital banking security. These processes help establish the legitimate identity of customers and mitigate risks associated with fraud, money laundering, and terrorist financing.

Digital banks utilize various methods for user verification, including one-time passwords (OTPs), biometric authentication (fingerprint and facial recognition), and knowledge-based authentication.

KYC procedures involve collecting and verifying customer identification documents, such as passports or driver’s licenses, and often include address verification. Digital banks leverage technology to automate and streamline these processes, often using electronic KYC (eKYC) systems.

Fee Structures in Digital Banking

Digital banks often employ different fee structures compared to traditional banks. Transparency is key. Customers should easily understand the fees associated with their accounts.

Common fee types include monthly maintenance fees, which some banks waive based on minimum balance requirements. Overdraft fees are another potential charge. ATM fees, especially for out-of-network withdrawals, are common, although some digital banks offer reimbursements.

Some digital banks also charge for international transactions or other specialized services. It’s crucial to carefully review the fee schedule before opening an account to avoid unexpected costs.

Limitations You Should Know

While digital banks offer numerous advantages, it’s crucial to be aware of their limitations. One key constraint is the lack of physical branches. This can be inconvenient for customers who prefer in-person banking services, such as depositing cash or complex transactions.

Another potential limitation involves customer service accessibility. Although many digital banks offer 24/7 online support, some customers may find navigating technical issues or resolving complex problems more challenging without face-to-face interaction. Furthermore, certain services, like notary services or certified checks, may not be readily available.

Finally, internet access dependency is a significant limitation. Customers without reliable internet access may find managing their finances challenging with a digital bank.

Case Study: Rise of Digital Banks in Europe

The European banking landscape has undergone a significant transformation with the rise of digital banks. These challenger banks, unburdened by legacy systems and physical branches, have quickly gained traction with tech-savvy consumers.

Several factors contributed to this growth. Increased smartphone penetration and evolving customer expectations towards digital-first services created a fertile ground for disruption. Favorable regulations like PSD2 further fueled competition and innovation within the financial sector.

Key players like Starling Bank, Nneo, and Revolut offer a range of services from basic account management to sophisticated investment tools, often at lower fees than traditional banks. This has put pressure on established institutions to adapt and enhance their digital offerings.

Future Outlook of Digital Finance

The future of digital finance appears poised for continued growth and transformation. Several key trends are expected to shape the landscape.

Increased Personalization: AI and machine learning will likely drive highly personalized financial services, offering tailored products and advice.

Enhanced Security: Biometric authentication and blockchain technology promise to strengthen security and reduce fraud.

Greater Financial Inclusion: Digital finance has the potential to reach underserved populations, providing access to essential financial services.

Embedded Finance: Financial services will become increasingly integrated into everyday platforms and applications, creating seamless experiences.

{kind=link}