Deciding whether to open a joint bank account is a significant financial step for any couple. A joint bank account allows both partners to deposit and withdraw money, offering shared financial responsibility and transparency. However, it’s crucial to carefully weigh the pros and cons of a joint bank account before making a decision. Understanding the implications of a joint bank account, such as its impact on credit scores, individual financial autonomy, and potential legal complexities is essential. This article will explore the key considerations to help you determine if a joint bank account is the right choice for your financial situation.

Managing finances as a couple can be challenging, and choosing the right banking arrangements is crucial for a healthy financial partnership. This article provides a comprehensive guide to help you navigate the decision of opening a joint bank account. We will explore the advantages and disadvantages of joint bank accounts, addressing common concerns such as liability, access, and control. We will also discuss alternative approaches, like maintaining separate accounts or using a combination of joint and individual accounts. By examining these factors, you can make an informed decision about whether a joint bank account aligns with your financial goals and relationship dynamics.

What Is a Joint Bank Account?

A joint bank account is a bank account owned by two or more people. Each account holder has equal access to the funds and can deposit, withdraw, and manage the account as if they were the sole owner.

This type of account differs from an individual account, which is owned and controlled by a single person. Joint accounts are often used by couples, family members, or business partners who wish to share financial responsibilities and resources.

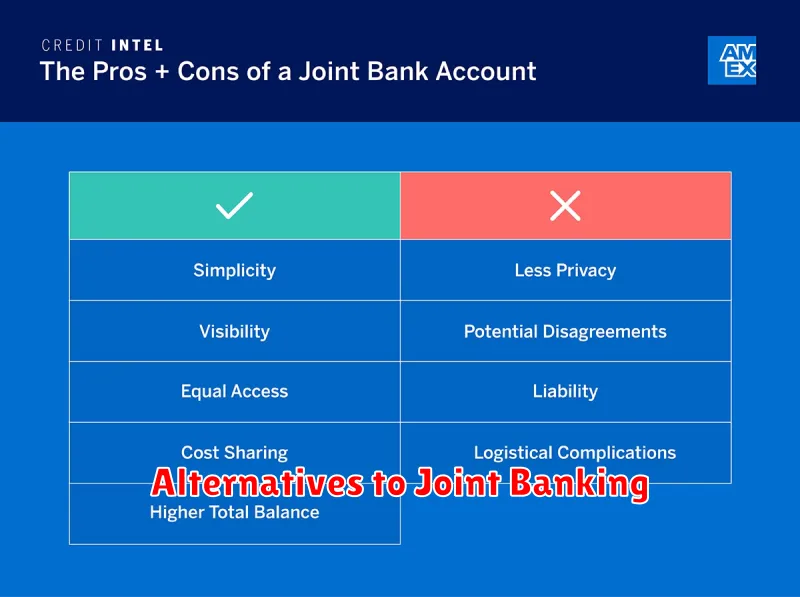

Pros of Having One

A joint bank account offers several advantages for managing shared finances. Transparency is a key benefit, as both account holders have full access to transaction history and balances. This can foster trust and open communication about spending habits.

Simplified bill payment is another advantage. With shared funds readily available, paying household expenses, mortgages, or rent becomes a streamlined process. It also simplifies large purchases that require combined resources.

In the event of an emergency or the incapacitation of one account holder, access to funds is maintained. This can prove crucial for covering necessary expenses.

Common Uses for Joint Accounts

Joint accounts offer convenient shared access to funds, making them suitable for various purposes.

Managing household expenses is a primary reason couples opt for joint accounts. Pooling resources simplifies bill payments and budgeting.

Elderly individuals often add a trusted family member to their accounts to assist with managing finances, ensuring bills are paid and funds are accessible when needed.

Business partnerships may utilize joint accounts for operational expenses, allowing both partners to access and manage funds.

When It Becomes Risky

While joint accounts offer convenience, they also present potential risks. A significant risk involves shared financial liability. If one account holder incurs debt, creditors can potentially access the entire joint account balance, regardless of who incurred the debt. This can be particularly problematic in cases of divorce, separation, or disagreements.

Another risk arises with the lack of individual control. Each account holder typically has full access to the funds, meaning one individual could deplete the account without the other’s knowledge or consent. This lack of transparency and control can strain relationships and create financial instability.

Furthermore, the death of one account holder can create complications. Depending on the type of joint account, the surviving owner may automatically inherit the funds, potentially bypassing estate planning wishes. This can be a source of conflict with other beneficiaries.

Alternatives to Joint Banking

If a joint account isn’t suitable, several alternatives exist to manage shared finances. Authorized users on an individual account permit another person to use the account, but the primary account holder retains ultimate control and responsibility. This approach is simpler to set up than a joint account, yet provides less financial autonomy for the authorized user.

Another option involves maintaining separate individual accounts and establishing clear agreements on shared expenses. This method preserves individual financial independence and can foster open communication about money management. Couples or housemates often utilize this strategy, allocating percentages or specific bills to each person.

For specific purposes, such as healthcare or estate planning, a power of attorney can grant designated individuals the legal authority to manage finances on behalf of another. This powerful tool requires careful consideration and typically involves legal documentation.

How to Open a Joint Account

Opening a joint account typically involves a straightforward process. First, choose a financial institution that meets your needs. Then, gather the necessary documentation. This usually includes valid government-issued identification, such as a driver’s license or passport, and Social Security numbers for all parties involved.

Next, visit a branch or apply online, if available. You’ll complete an application form providing personal information for each account holder. Finally, make the initial deposit as required by the institution. Once the application is processed, the account will be open and ready for use.

Communication Is Key

Opening a joint bank account requires open and honest communication with your partner. Clearly discuss your financial goals, spending habits, and expectations before making a decision. Miscommunication or avoiding difficult conversations about money can lead to conflict and resentment later on.

Regularly review your account activity together. This helps maintain transparency and allows both partners to stay informed about the account’s balance and transactions. Proactive communication about finances is crucial for a successful joint account experience.

Managing Contributions

Deciding how to contribute to a joint account requires open communication. Will you contribute equally, or proportionally based on income? A clear, upfront agreement can prevent future misunderstandings.

Tracking individual contributions can be beneficial, especially for unequal contributions. This doesn’t imply mistrust, but rather provides clarity for situations like separating finances or understanding individual spending habits.

Automating transfers can simplify regular contributions. Setting up recurring transfers ensures consistent deposits and reduces the risk of missed payments.

Handling Account Closure

Closing a joint account requires the agreement of all account holders. All parties must sign the necessary documentation.

Upon closure, the remaining funds are typically distributed equally among the account holders, unless a different agreement is in place. It’s crucial to discuss and agree upon the distribution of funds before initiating the closure process to avoid potential disputes.

Consider addressing the following before closing the account:

- Outstanding checks or automatic payments

- Direct deposits

- Transferring recurring bills to individual accounts

Legal Implications to Know

Opening a joint bank account creates certain legal rights and responsibilities for both account holders. Each individual typically has equal access to the funds and can deposit or withdraw money without the other’s permission. This shared access is a key consideration, particularly in situations of disagreement or relationship breakdown.

Creditor access is another important legal aspect. Creditors of one account holder may be able to access the joint account funds to satisfy debts, even if the debt was incurred solely by one individual. Understanding these implications beforehand can prevent future complications.

Upon the death of one account holder, the surviving owner typically assumes full ownership of the account’s assets, often bypassing probate court. This process, however, can be affected by existing wills or state laws.

{kind=link}